Disclosure: This is a partnered post with Tangerine Bank. However, all opinions and views on this post are 100% my own.

When I think of February, I think about RRSPs. Well I used to only think about RRSPs, but now I also think about TFSAs as well, and the rest of my investments. If you have been contributing to your RRSP or TFSA throughout the year, then you will be fine. If you have not, then you need to make your contributions by March 2, 2020 for your 2019 tax year. Have you ever wondered which is better? Well, that really depends. RRSPs were created in 1957 as a way to encourage Canadians to save for Retirement. in 2009, The federal government created the TFSA as another way for Canadians to invest their money. Let’s first review what RRSPs and TFSAs are.

RRSPs

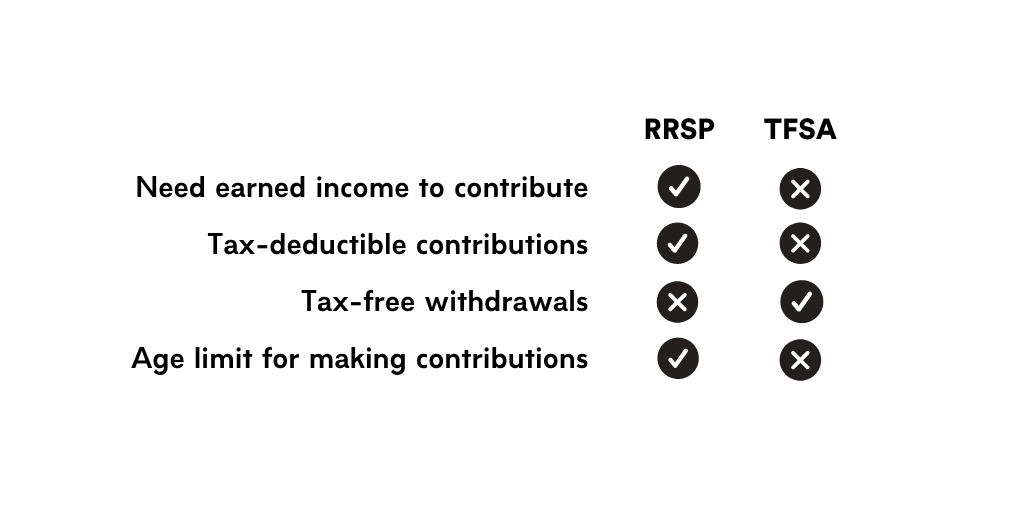

RRSP stands for Registered Retirement Savings Plan. You set yup your RRSP through a finanical institution. An RRSP is a retirement savings plan that you establish, that we register, and to which you or your spouse or common-law partner contribute. Deductible RRSP contributions can be used to reduce your tax. Any income you earn in the RRSP is usually exempt from tax as long as the funds remain in the plan; you generally have to pay tax when you receive payments from the plan. You must have “earned income” to contribute to an RRSP. To start building RRSP contribution room, you have to file an income tax return — even if you don’t owe any tax. Your notice of assessment will tell you how much money you can put into your RRSP each year.

RRSP Contribution Limits

Contribution limits are calculated at 18% of the prior year’s reported earned income (from employment or self-employment), up to a maximum. The maximum contribution amount for 2019 is $16,200. Since 2010 it has been indexed to the annual increase in the average wage.

TFSAs

TFSA stands for Tax-Free Savings Account. The TFSA program began in 2009. It is a way for individuals who are 18 and older and who have a valid social insurance number to set money aside tax-free throughout their lifetime. Contributions to a TFSA are not deductible for income tax purposes. Any amount contributed as well as any income earned in the account (for example, investment income and capital gains) is generally tax-free, even when it is withdrawn. Administrative or other fees in relation to TFSA and any interest or money borrowed to contribute to a TFSA are not tax deductible. insurance number

Generally, the types of investments that are permitted in a TFSA are the same as those permitted in a registered retirement savings plan (RRSP). These would include:cash, mutual funds, securities listed on a designated stock exchange, guaranteed investment certificates, bonds, certain shares of small business corporations.

TFSA Contribution Room

The TFSA contribution room is made up of the total of all of the following:your TFSA dollar limit, any unused TFSA contribution room from previous years, any withdrawals made from the TFSA in the previous year.

#DYK If you have never opened a TFSA, you can contribute $69,500!

Any contributions that are made or withdrawn from a TFSA in the prior year may not be reflected in your available current year contribution room until after the end of February. All issuers have until the last day of February to electronically submit a TFSA record to the CRA for each individual who has a TFSA. Any transactions made in the current year will not be included. You do not need to include TFSA information on your tax return because they are neither taxable or deductible. You will be penalized however, if you go over your contribution limit.

RRSPs vs TFSA

Preet Banerjee explains the differences between RRSPs and TFSAs.

The main difference between an RRSP and TFSA is the timing of taxes:

- An RRSP lets you defer taxes – an advantage if your marginal tax rate

is lower in retirement. - With a TFSA, you’ve already paid tax on the money you contribute – an advantage if your marginal tax rate

is higher when you withdraw the money.

Join the Conversation on Twitter

If you want to talk about RRSPs, TFSAs and investing, then you should join the Tangerine Bank Invest Savvy chat. Brian Ong from the Tangerine Bank Investments Funds Team will be answering questions

Date: Tuesday, February 4, 2020

Time: 8:00pm ET – 9:00pm ET

Twitter Party Host: @TangerineBank

Twitter Party Guest: Brian Ong from the Tangerine Bank Investments Funds Team will be available to answer your questions

Twitter Party Moderator: @ShesConnected

Prizing: $500 in gift cards

Hashtag: #InvestSavvy

Rules & Regs http://bit.ly/38yIOt4

Anyone can participate in the Twitter chat, however only those who live in Canada excluding the province of Quebec can win prizes.

Twitter Chat Questions

1) Are you currently investing? If not, what’s preventing you?

2) Do you understand the differences between an RRSP/RSP and a TFSA?

3) How hands on are you with your investments? Do you have a financial advisor?

4) Do you know what’s meant by the term MER, and how it relates to an investment’s management fees?

5) How do you feel about investing and retirement planning?

6) Are you currently saving for retirement? If not, what’s preventing you?

7) Do you have a retirement savings tip to share?